In India's rapidly evolving fintech landscape, the Unified Payments Interface (UPI) has emerged as a game-changer, propelling the country to the forefront of digital payment innovation. This transformation is not just about technology but a paradigm shift in consumer behavior, financial inclusion, and creating a digital economy accessible to millions of Indians.

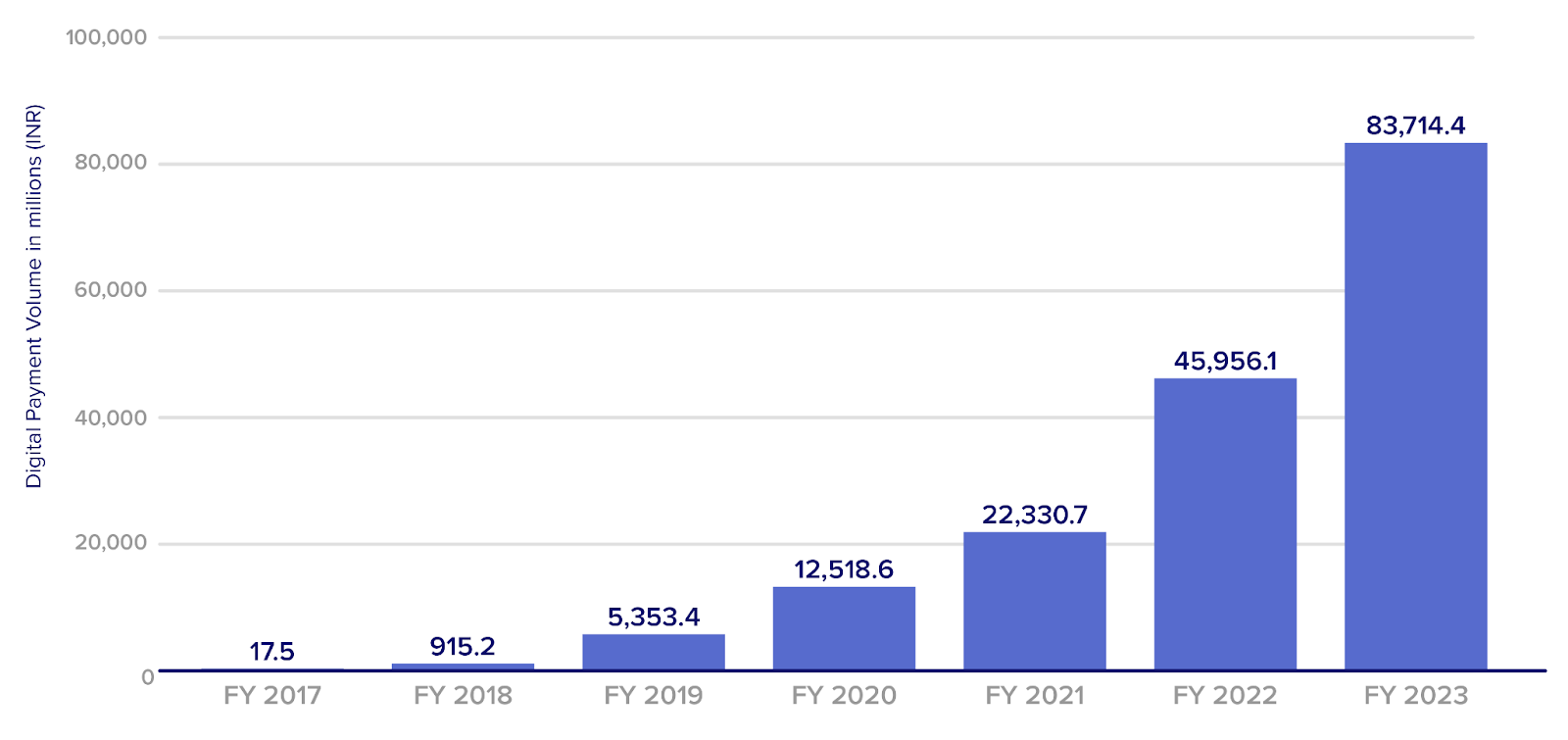

The volume of UPI-based digital payments in India was over 83 billion in the financial year 2023, a significant increase from the previous year's value of around 45 billion.

This widespread adoption of UPI is mainly due to its ease of use. Through UPI, people can make instant bank-to-bank transactions using only their mobile phone number and a unique PIN (MPIN), which makes financial transactions extremely simple.

UPI in India

UPI is an advanced payment system that allows the transfer of money between any two parties' bank accounts through a mobile platform. Developed by the National Payments Corporation of India (NPCI), UPI operates over the Immediate Payment Service (IMPS) infrastructure, enabling round-the-clock money transfers.

Key features of UPI

- Real-time transfers: Leveraging the IMPS infrastructure, UPI enables instant transfers, making it highly efficient for all kinds of transactions.

- Single interface for multiple accounts: Multiple bank accounts can be linked to a single mobile application, allowing users to manage their finances seamlessly.

- Secure transactions:: UPI ensures security through a combination of factors, such as the mobile device and the UPI PIN, making transactions safe and user-friendly.

- Simplicity: UPI allows users to create a Virtual Payment Address (VPA) or UPI ID, eliminating the need to remember and enter bank account details or IFSC codes for each transaction.

- Interoperability: UPI facilitates transactions across banks and UPI-enabled apps, promoting a unified ecosystem.

The role of APIs in the UPI framework

The true potential of UPI is unlocked through Application Programming Interfaces (APIs), which act as digital bridges, enabling businesses to integrate UPI into their applications and platforms. This integration allows them to accept payments directly from their customers, streamlining the transaction process and enhancing customer experience. UPI and API integration paves the way for a faster, more convenient, and secure payment ecosystem in India.

APIs in the UPI ecosystem provide a standardized way for software components to interact, allowing for the initiation, authorization, and processing of payments across different banking institutions and payment platforms. These APIs ensure that despite the diversity of banks and their underlying systems, transactions can be conducted smoothly and securely, offering a unified user experience.

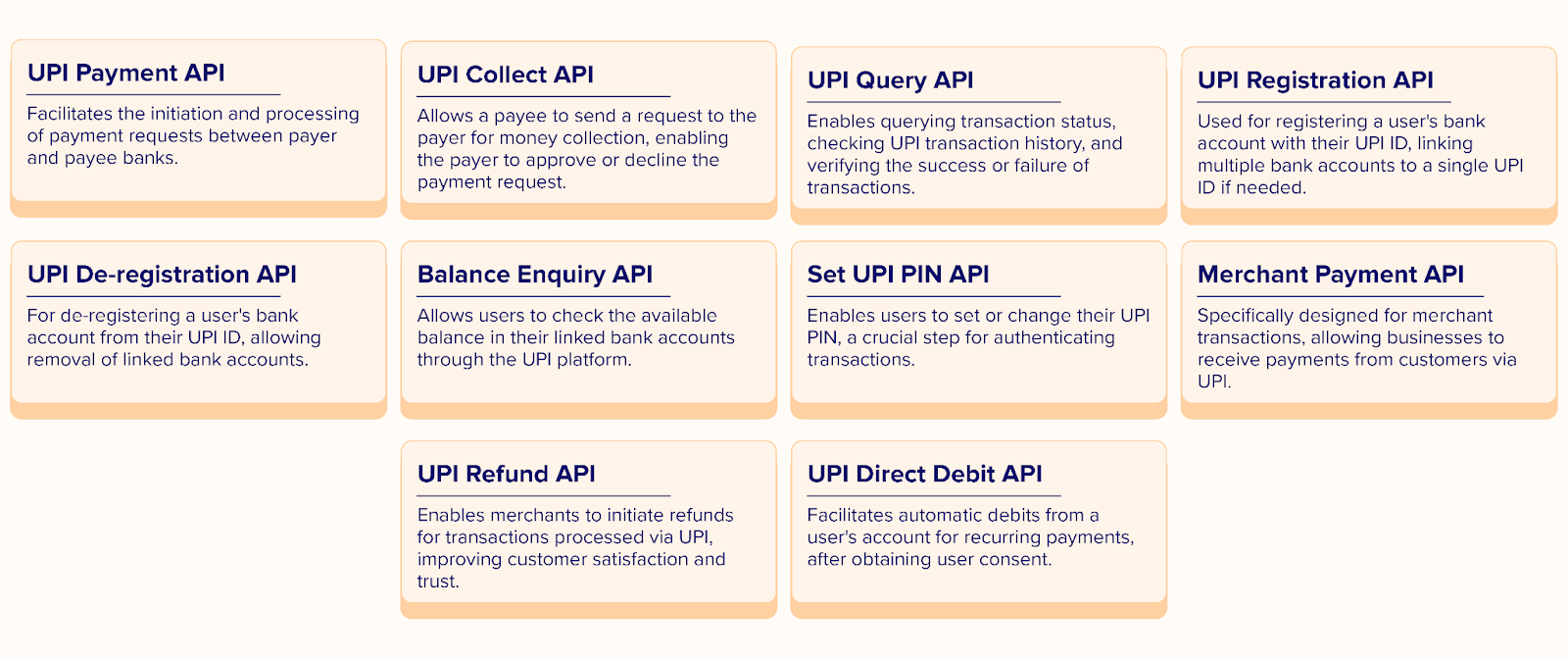

Different UPI APIs

UPI offers a suite of APIs that enable a wide range of financial transactions and services. From initiating payment requests between banks to enabling users to check their account balances, these APIs provide the crucial infrastructure needed for seamless, real-time financial exchanges. They allow for the easy integration of UPI's functionalities into various banking and merchant platforms, broadening the scope of digital transactions across the country. Whether it's for peer-to-peer money transfers, bill payments, or merchant transactions, UPI's APIs ensure that every transaction is secure, swift, and user-friendly. Here's a list of some of the key UPI APIs:

These APIs (along with others) form the backbone of the UPI ecosystem, enabling a secure, efficient, and interoperable framework for digital payments across various platforms and services in India.

Best practices in API lifecycle management for UPI services

Adhering to best practices in API lifecycle management is crucial to ensure the robustness, security, and scalability of UPI services. Here are a few:

- Version control: Implementing strict version control is essential to manage updates and modifications to APIs without disrupting existing services. It involves maintaining backward compatibility and providing clear documentation to developers and stakeholders.

- Traffic management: As UPI transactions grow exponentially, API traffic becomes critical. Techniques such as rate limiting, caching, and load balancing can help efficiently manage request loads, ensuring high availability and consistent performance.

- Security protocols: Security is crucial in the UPI framework, given the sensitivity of financial transactions. Implementing robust security protocols such as OAuth for authentication, SSL/TLS for secure communication, and encryption for data at rest and in transit is non-negotiable. Regular security audits and compliance checks with industry standards like PCI DSS are also essential.

- Monitoring and analytics: Continuous monitoring of API performance and usage analytics can provide insights into operational efficiencies, user behavior, and potential security threats. This proactive approach enables identifying and resolving issues before they impact the service.

- Developer ecosystem support: Providing comprehensive documentation, developer tools, and sandbox environments can foster a vibrant developer ecosystem around UPI APIs. This support accelerates innovation and the integration of UPI services into a wide array of applications.

Enhancing UPI transactions with advanced API strategies

Adopting advanced API strategies is essential to amplify UPI’s benefits. These strategies can significantly enhance UPI transaction speeds, minimize failure rates, and elevate the user experience. Here are are few strategies that can improve UPI transactions:

Optimizing API integration for improved speed and reduced failures

- Efficient API caching: Smart caching of frequently accessed data reduces backend system load, speeding up transaction processing. Services become more responsive and efficient by storing responses for common queries, such as balance inquiries and transaction status checks.

- Adaptive retry mechanisms: Implementing intelligent retry algorithms can mitigate the impact of temporary issues like network latency or server downtime, increasing transaction success rates without straining the system.

- Concurrency and load management: Enhancing the API infrastructure to manage multiple transactions simultaneously can decrease failure rates. Techniques include employing load balancers, optimizing database access, and utilizing asynchronous processing to maintain performance during peak volumes.

- API throttling and rate limiting: These measures prevent system abuse and ensure fair resource distribution by controlling the number of requests a user can make in a specific timeframe, thus maintaining system stability and reliability under high demand.

Leveraging API analytics to enhance user experience

- Transaction pattern analysis: Analyzing transaction patterns through API analytics provides insights into user behavior, helping predict peak times, identify bottlenecks, and take measures to handle increased loads, improving the user experience.

- Customization and personalization: Insights from API analytics allow for the tailoring of the UPI experience to meet individual user needs. Introducing personalized features based on user activity, such as transaction limits or favorite contacts, makes interactions more intuitive.

- Fraud detection and security enhancements: Advanced analytics play a crucial role in early detection of fraudulent transactions and security threats. Monitoring unusual patterns enables swift action to mitigate risks, safeguarding the UPI ecosystem.

- Feedback loop for continuous improvement: A feedback mechanism using API analytics facilitates the continuous refinement of UPI services. Close monitoring of API performance and user feedback helps address issues and introduce features that respond to users' evolving needs.

Enhancing security protocols for robust protection

- Robust authentication mechanisms: Implementing multi-factor authentication (MFA) and stronger encryption methods for data in transit and at rest can significantly elevate the security level of UPI transactions. This ensures that even if data is intercepted, it remains unreadable and secure.

- Regular security audits and compliance checks: Conducting regular security audits and ensuring compliance with the latest financial and data protection regulations can help identify and mitigate potential security risks before they can be exploited. These audits can pinpoint weaknesses in the API infrastructure and suggest improvements to strengthen the system against attacks.

- Real-time monitoring and anomaly detection: Utilizing real-time monitoring systems to track transaction flows and detect anomalies can provide immediate alerts on suspicious activities. This enables quick response to potential security threats, minimizing the risk of fraud and unauthorized access.

- Secure API gateway implementation: Deploying a secure API gateway can act as a robust intermediary between clients and backend services, offering an additional layer of security. This gateway can manage authentication, monitor traffic for suspicious patterns, and enforce security policies, ensuring that only legitimate requests are processed.

- End-to-end encryption for sensitive data: Ensuring that sensitive data, such as personal identification information and transaction details, is encrypted from the point of initiation to the final destination adds a strong layer of security. This practice protects user data against interception and misuse throughout the transaction process.

Building a future-proof UPI infrastructure

India's UPI is going global, with many countries adopting this seamless payment system, showcasing India's rising influence in digital finance. This expansion is paving the way for streamlined cross-border transactions, enhancing global financial connectivity. Looking ahead, the strength and adaptability of UPI's framework will rely on embracing next-gen technologies such as AI and blockchain.

AI stands to revolutionize UPI transactions with smarter security measures and tailored user interactions, while blockchain technology offers unmatched transparency and reliability through decentralized record-keeping. Furthermore, the evolution of payment systems will lean heavily on developing more sophisticated APIs and the scalability of Integration Platforms as a Service (iPaaS). These innovations will not only enhance transaction security and speed but also ensure UPI can easily support an expanding volume of payments across borders. Careful integration and management of these technologies are crucial for UPI, preparing it to meet tomorrow's digital payment needs. UPI is well-positioned to continue its growth through strategic adoption of these advancements, solidifying its role in India's digital payment ecosystem.