We buy insurance while booking a flight, pay for groceries within the food delivery app, and send money to a friend directly from the messaging app. This is the magic of embedded finance – weaving financial services seamlessly into the fabric of your everyday life.

The financial landscape has witnessed a transformative shift in recent years, redefining how consumers and businesses interact with financial services. At the heart of this transformation is embedded finance - integrating financial services into non-financial platforms and applications, enabling companies to offer financial products directly within their ecosystems.

The growing popularity of embedded finance in India

The growth of embedded finance in India has been skyrocketing, owing to the country's widespread digital adoption and a booming fintech ecosystem. This growth is further propelled by the Indian population's increasing demand for convenient and accessible financial services integrated seamlessly into their daily digital interactions.

The Indian embedded finance ecosystem is expected to grow at a CAGR of 30.4% over the period of 2022–29, generating a revenue of USD 21.12 billion.

APIs are central to the acceleration of embedded finance innovation in India, enabling the seamless integration of financial services into various digital platforms. They are the unsung heroes of the fintech world, working behind the scenes to facilitate real-time transactions, personalize financial offerings, and ensure that financial operations are conducted smoothly and securely.

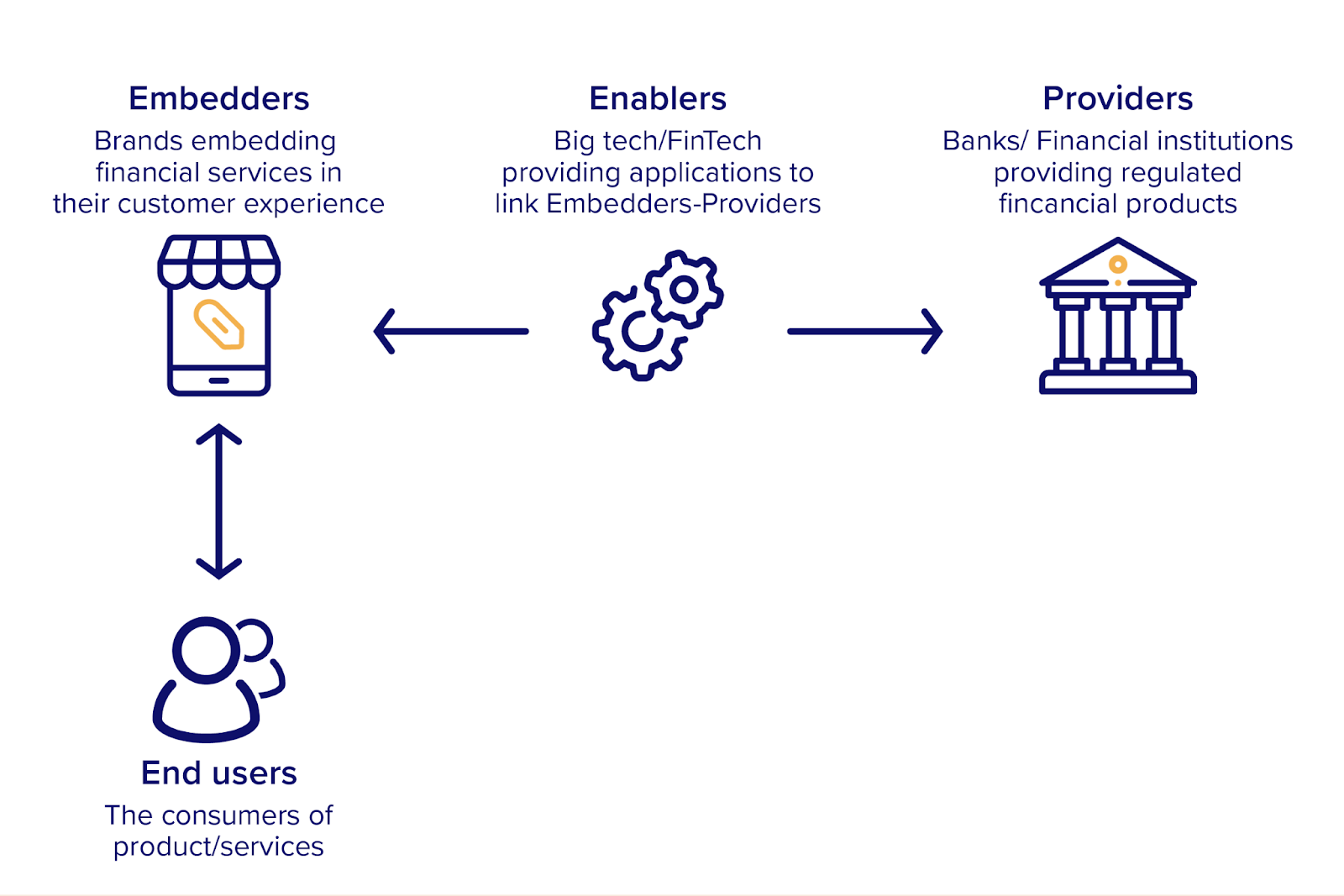

APIs - the backbone of embedded finance

Embedded finance is blending financial services into everyday non-financial apps and websites.

Financial institutions, including banks, fintech companies, and NBFCs, offer APIs that enable seamless integration of financial functionalities- payments, lending, insurance, and investment services directly into non-financial consumer applications and platforms. These range from e-commerce platforms and retail companies to tech startups and social media platforms, essentially any entity looking to embed financial services into their existing digital ecosystem.

This integration facilitates a seamless and cohesive user experience, allowing consumers to access and utilize financial services within the interfaces of the platform they are in without the need for direct interaction with banks or traditional financial providers. The result is a frictionless, intuitive financial experience that meets users where they are, dramatically enhancing accessibility and convenience.

Popular use cases of embedded finance in India's financial sector include online payment options at the point of sale (embedded payments), real-time insurance bundling during transactions (embedded insurance), API-driven access to investment platforms (embedded investments), direct provision of card services (embedded cards), and Buy Now, Pay Later offerings (embedded lending).

Consumer: Individuals who buy non-financial products and may become potential users of embedded financial services, sometimes without immediate identification as clients.

Business: Entities selling non-financial goods or services to consumers.

Financial institutions (Banks, NBFCs, Fintechs): Organizations offering financial products indirectly to consumers through partnerships with businesses rather than direct sales.

Embedded finance offers banks and traditional financial institutions unprecedented growth opportunities and avenues for innovation, enabling them to tap into new customer segments and deliver financial products through diverse digital platforms.

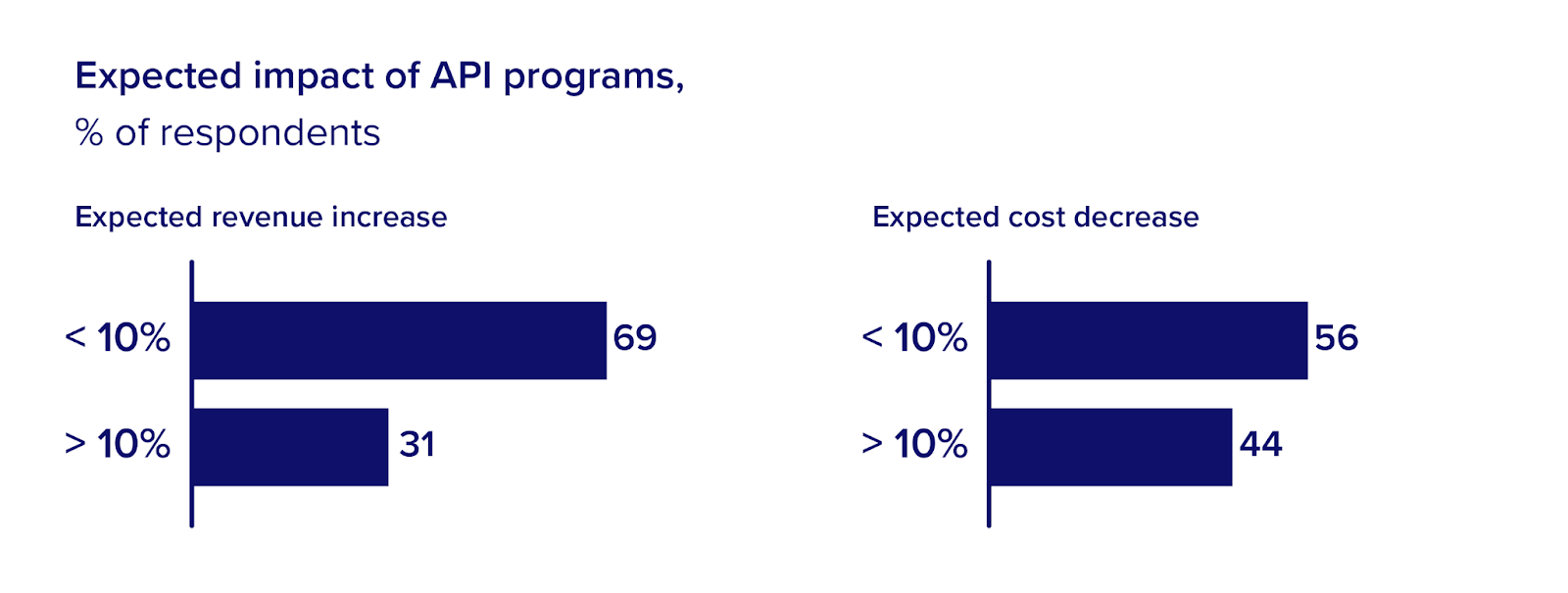

According to McKinsey, the focus of API deployment in banking has shifted from simplifying IT operations to sparking innovation and driving revenue growth.

For fintech companies, it presents a fertile ground for growth, allowing them to disrupt the market with novel solutions and collaborations that extend financial services to previously unreachable audiences.

Key impact areas of embedded finance

Enhancing user experience through embedded finance

Increased convenience and accessibility: With more and more apps becoming a part of consumers' daily lives, the preference to have “everything in one place” is growing more than ever. Embedded finance eliminates the need for consumers to switch between multiple apps or websites to access financial services. Whether it's making a payment, applying for a loan, or investing, these services become accessible within the platforms consumers already use daily.

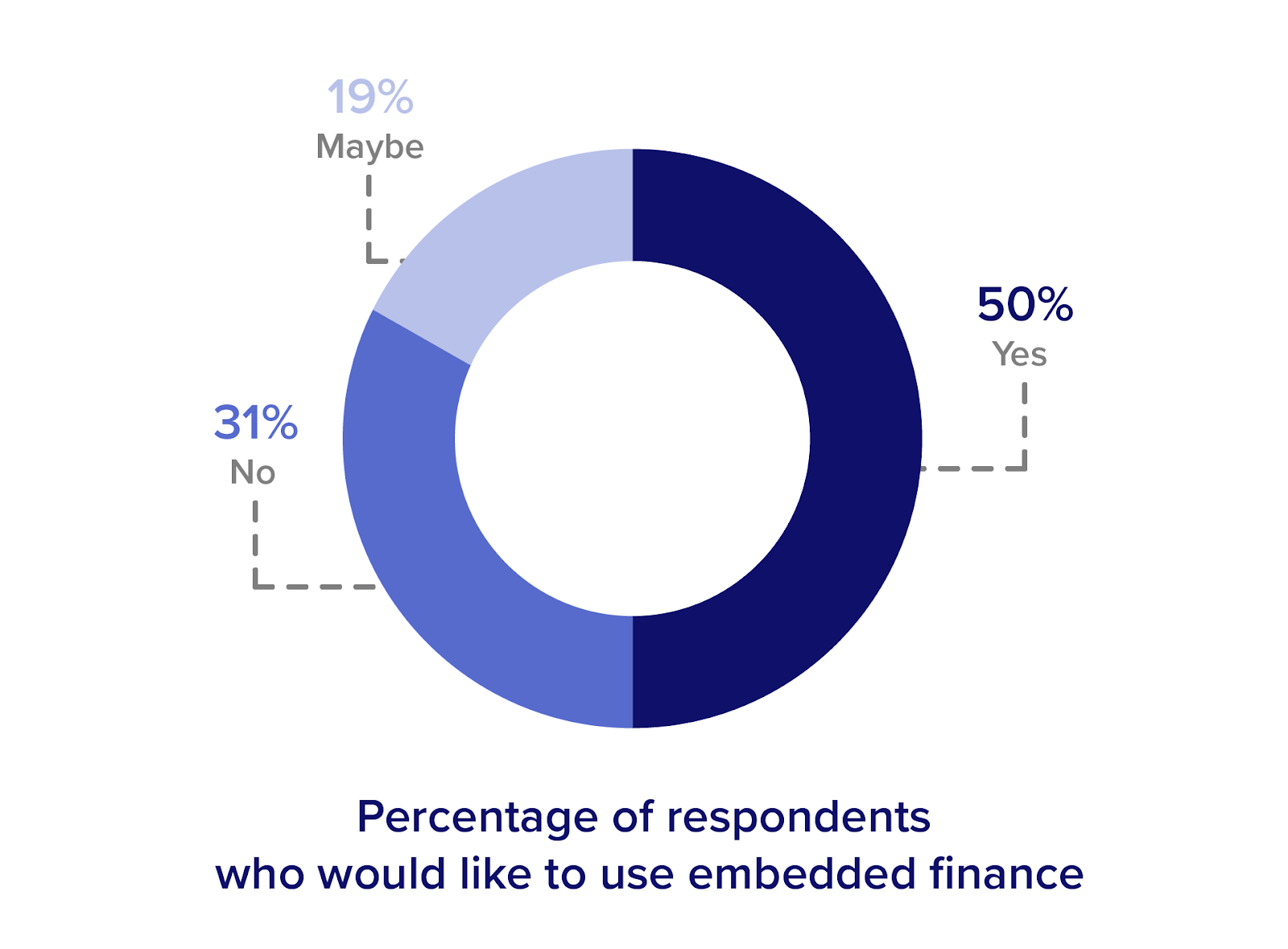

According to How India Borrows survey, 50% of respondents from 17 cities (including tier-1 and tier-2) across India would like to use embedded finance.

Personalized financial services: By integrating financial services into consumer platforms, there's a greater capacity for personalization. Consumers receive financial product recommendations and services tailored to their buying behavior and preferences, enhancing their overall experience.

Enhanced security: Embedded finance often comes with robust security measures, leveraging the advanced security protocols of the platforms they are integrated with. This means consumers can benefit from secure financial transactions without the hassle of extra security steps.

Empowering non-financial businesses with new opportunities

Improved customer engagement and retention: Providing financial services directly on the platform increases the value offered to the customer, improving engagement and loyalty. A seamless and integrated experience reduces friction, potentially increasing sales and customer retention.

Competitive advantage: Embedding financial services can differentiate a non-financial business from its competitors, offering consumers a more comprehensive and convenient service package.

New revenue streams: Non-financial sector businesses can use their existing infrastructure, data, and customer base to introduce financial services products, thereby boosting revenue through sourcing and distribution. This could be through transaction fees, commissions, or even premium services that enhance the customer's buying experience. This approach not only increases their profitability but also improves the customer experience and fosters loyalty.

Broadening horizons for financial service providers

Expanded market reach: Financial institutions can reach a broader audience by integrating their services into non-financial platforms. This partnership allows them to access customers who might not have engaged with their services directly.

Reduced customer acquisition costs: Leveraging the customer base of non-financial platforms, financial service providers can significantly reduce the costs of acquiring new customers.

Innovation and product development: Collaborating with non-financial businesses offers financial institutions insights into consumer behavior and preferences, driving innovation and enabling the development of new products and services more aligned with consumer needs.

Promoting financial inclusion and innovation

Democratizing finance: APIs facilitate the embedding of essential financial services into popular apps, reaching underserved and unbanked populations. This integration extends the benefits of the digital economy, fostering financial inclusion and empowerment.

Stimulating innovation and competition: APIs level the playing field, allowing startups to access financial infrastructure and compete with traditional institutions. This encourages a dynamic environment of innovation, improving services and products for consumers.

Conclusion

Embedded finance, already marking its territory as one of the fintech industry's most rapidly expanding segments, holds immense potential in India—a nation characterized by a large, internet-savvy, young demographic eagerly embracing digital solutions. Organizations that adeptly navigate this non-traditional financial environment, assessing the opportunities and challenges it presents and strategically harnessing the power of APIs are set to reap substantial benefits. Embracing this shift towards embedded finance promises enhanced market penetration and customer engagement and heralding a new era of corporate growth and financial democratization in India.