Banking has moved past the traditional bank buildings and become a part of our everyday digital life. This change isn't just happening in cities but also in India's rural areas, where it's hard to find a bank nearby. Now, even in small towns, people use technologies like scan-and-pay and tap-and-pay to handle their money. This digital leap forward has been possible because of the evolution of Banking as a Service (BaaS).

BaaS represents a semi-open banking model that enables organizations outside the banking sector to provide banking services to their customers. This model is paving the way for new possibilities for companies, including fintech startups and established players across various sectors, to deliver banking functions previously limited to traditional financial institutions.

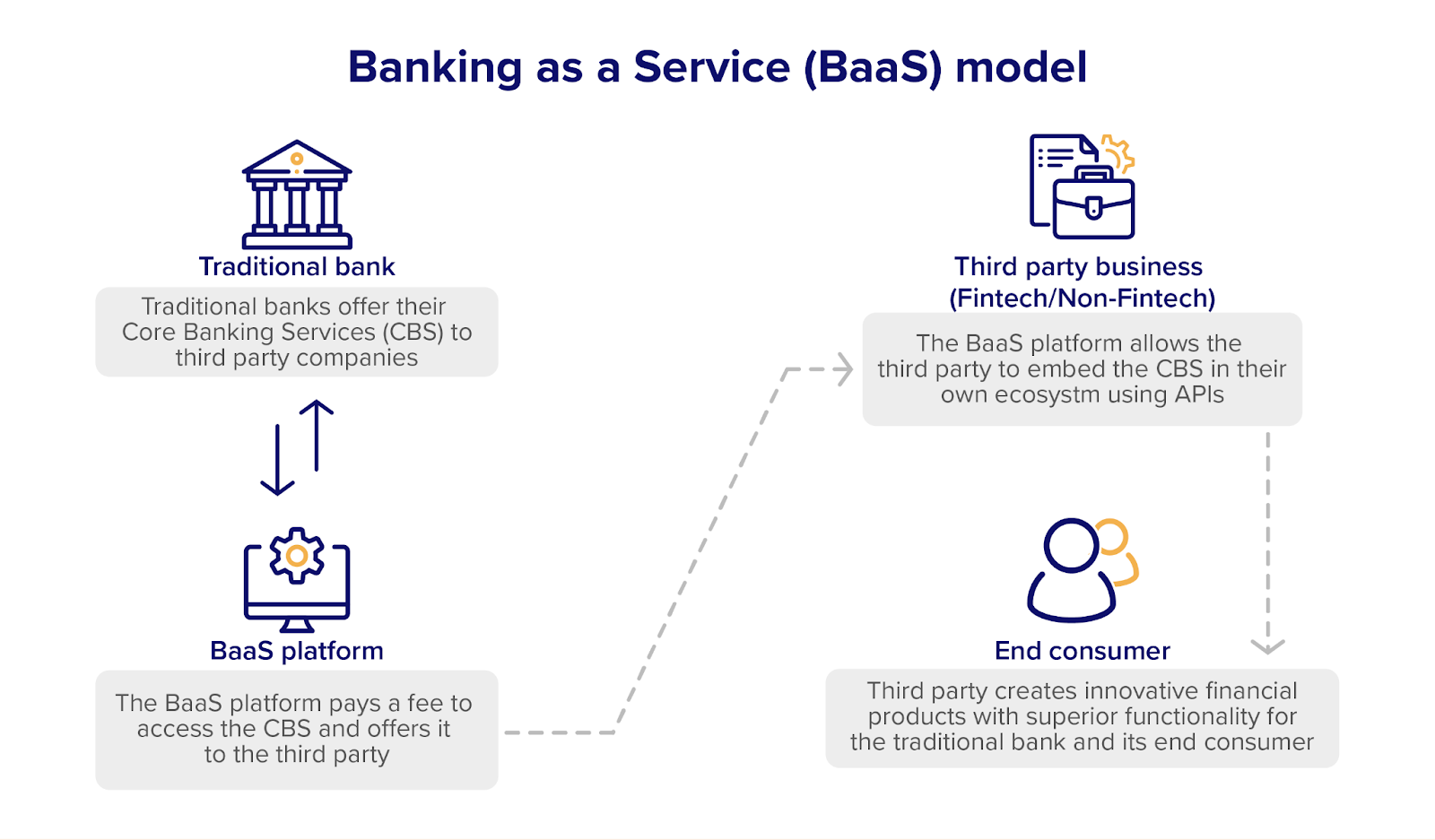

The BaaS model

The BaaS model involves banks creating and maintaining platforms that provide access to a range of banking functions through Application Programming Interfaces (APIs). This enables third-party companies, which do not possess banking licenses, to integrate services such as account management, payment processing, and loan offerings into their own offerings. As a result, these companies can seamlessly offer financial services to their clients, leveraging the established infrastructure and regulatory compliance of partnering banks, without having to navigate the complex process of becoming a bank themselves.

The current state of BaaS in India

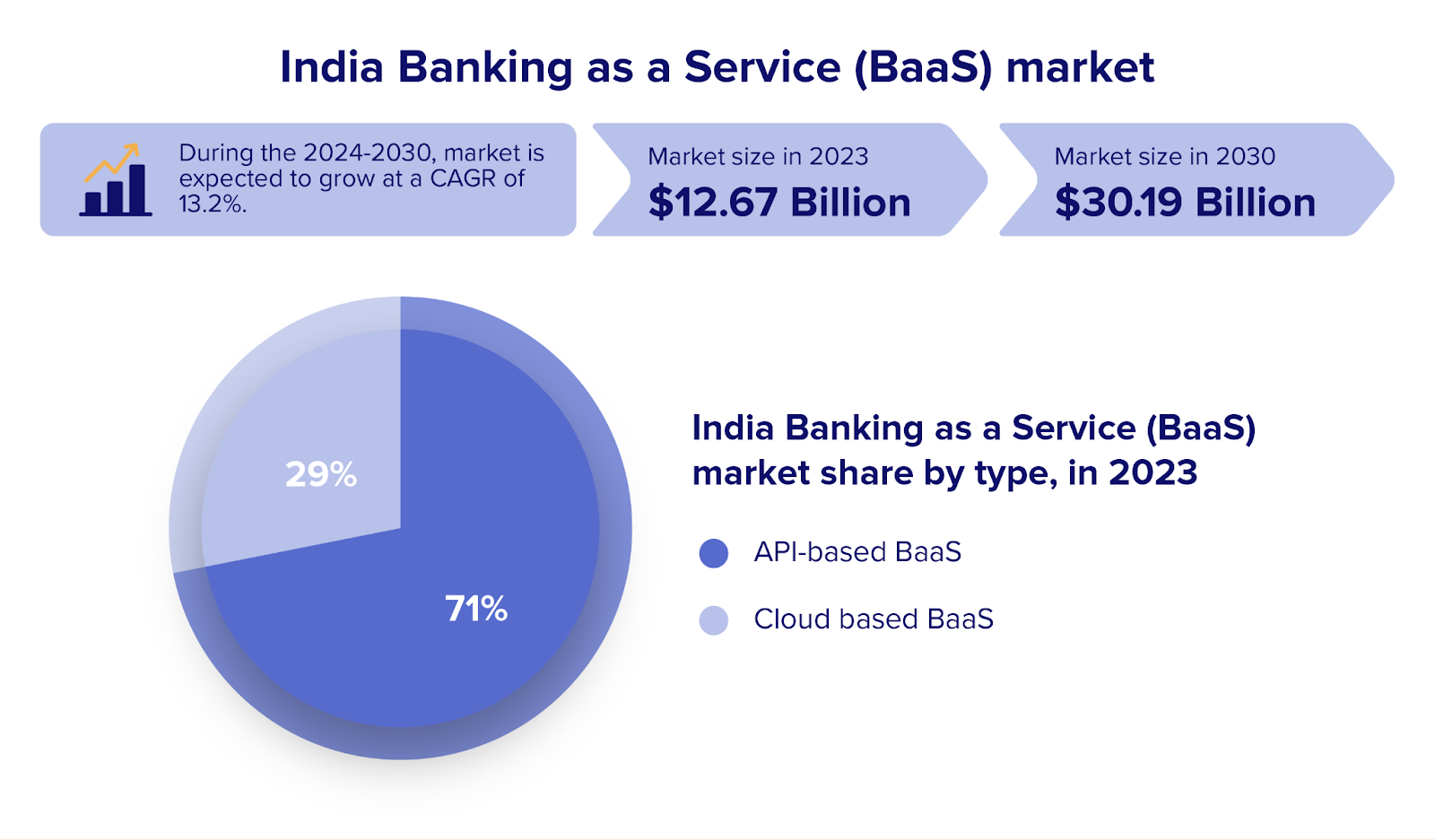

Indian BaaS Market size was valued at US$ 12.67 billion in 2023, and the total India BaaS revenue is expected to grow at 13.2% from 2024 to 2030, reaching nearly US$ 30.19 billion.

This remarkable growth is driven by several key factors, including the rapid development of the fintech sector, encouraging government initiatives and policies, and the widespread adoption of internet and smartphones throughout India. Given these dynamics, the Indian BaaS industry is on the verge of transforming the financial services sector, making innovative banking solutions accessible to millions of users across India.

Opportunities of BaaS in India

BaaS is revolutionizing the Indian financial landscape, providing great opportunities for enhancing financial inclusion, fostering innovation, empowering startups, and elevating the customer experience. Here are a few key opportunities for BaaS:

Enhance financial inclusion

A substantial segment of India's population is still unbanked or underbanked, particularly in rural and remote areas. As per the article Fintech sector catalysing India's growth story among unbanked population, until March 2023, 190 million Indians were still unbanked. BaaS has the potential to bridge this gap by leveraging digital platforms to extend essential banking services to these regions through some key financial services like-

- Microfinance and lending: Fintech startups leveraging BaaS make microloans accessible to small businesses and individual borrowers in underserved areas. This approach democratizes access to finance, allowing those in remote locations to receive the capital they need to grow.

- Savings and accounts: BaaS facilitates the creation of simplified savings accounts that do not require a minimum balance. These accounts enable basic banking operations, including money transfers and bill payments, essential for fostering financial literacy and encouraging saving practices among populations without traditional bank access.

- Insurance penetration: BaaS platforms can collaborate with insurance providers to offer micro-insurance products designed for the underserved. These products cover specific risks, such as health emergencies, accidental death, and crop failure, offering a crucial safety net for those in vulnerable situations.

Foster innovation in financial services

BaaS democratizes access to banking infrastructure, enabling fintech startups to develop and deploy cutting-edge innovative financial products swiftly. Among the standout innovations are co-branded credit cards, which offer tailored rewards and benefits in partnership with brands outside the traditional banking sector, and Buy Now, Pay Later (BNPL) schemes that provide flexible payment options for consumers, enhancing the affordability of purchases and facilitating smoother transactions. Personal finance management tools that leverage AI to offer budgeting advice and savings strategies are becoming increasingly popular, demonstrating the vast potential for BaaS to innovate beyond conventional banking boundaries.

Strengthen the startup ecosystem

BaaS significantly reduces entry barriers for new fintech startups, providing them with the infrastructure needed to innovate and scale. This fosters a symbiotic relationship between traditional banks and agile startups, driving mutual growth and innovation.

- Reduced operational costs and faster market entry: Startups benefit from BaaS by avoiding the hefty investments required for developing proprietary banking systems. This advantage, coupled with streamlined regulatory compliance facilitated by BaaS partnerships, enables startups to launch their services more swiftly and cost-effectively.

- Scalability and flexibility: The scalable nature of BaaS infrastructure ensures that startups can grow their operations without the burden of significant infrastructural investments. This agility allows startups to adapt to market demands, expanding their reach and enhancing their impact on the financial ecosystem.

Enhance customer experience

In today's digital age, customer’s expectations for personalized banking services are higher than ever. BaaS is at the forefront of meeting these demands by revolutionizing how customers interact with financial services.

- Personalized financial services: BaaS platforms leverage the power of data analytics and AI to offer personalized banking solutions. By analyzing individual user data, these platforms can tailor financial products and services to meet each customer's unique needs. This level of personalization not only improves the functionality of the user interface but also broadens accessibility through multi-language support, ensuring that a wider range of customers can benefit from these services.

- Seamless integration and 24/7 access: BaaS seamlessly integrates financial services across various digital platforms and applications, allowing customers to manage their finances through a single, unified interface, eliminating the need to navigate between multiple apps or websites. Moreover, providing 24/7 access means that customers can perform banking transactions, access account information, and receive support whenever they need it, regardless of their location or time zone. This around-the-clock availability significantly enhances the customer experience.

Improve efficiency and cost-effectiveness of financial services

Integrating BaaS into the financial ecosystem optimizes the way financial services are delivered and enhances the value provided to institutions and their customers.

- Better operational efficiencies: BaaS significantly enhances operational efficiencies by introducing cost-saving measures that benefit financial service providers. BaaS reduces the need for extensive manual processing and infrastructure maintenance by adopting outsourcing and employing automation technologies. This reduction in operational expenditure allows financial institutions to offer their services at more competitive prices, improving the quality and range of financial products available to consumers.

- Operational and consumer benefits: The streamlined operations facilitated by BaaS, combined with its scalable infrastructure, empower financial institutions to lower their transaction fees and offer more favorable terms on loans and savings accounts. Such efficiencies make financial services more cost-effective for the providers and more affordable and accessible for consumers.

Challenges of BaaS in India

While BaaS holds immense promise for transforming the Indian financial landscape, its path is strewn with various challenges. From regulatory complexities to the integration with legacy systems, each hurdle requires careful navigation. Here’s a list of a few key challenges:

Regulatory hurdles

The regulatory framework in India, while supportive of innovation, presents a complex landscape for BaaS operations. The RBI and other regulatory bodies have set stringent guidelines for financial services, aimed at protecting consumer interests and maintaining financial stability. However, the rapid evolution of BaaS often outpaces regulatory updates, leading to a gray area where BaaS providers seek clarity. For instance, the following circulars serve as recent instances of regulatory mandates imposed on banks.

- Master Direction on Outsourcing of Information Technology Services 2023, mandates financial institutions to maintain high standards in outsourcing IT services, focusing on risk management, data security, and regulatory compliance.

- Digital Personal Data Protection (DPDP) Act 2023, establishes a framework for personal data protection in the digital realm, outlining user rights, and setting standards for data handling by businesses

- Regulation of Payment Aggregator – Cross Border (PA-CB) 2023, provides a structured approach to managing cross-border payment aggregators, focusing on transparency, security, and compliance with global payment standards.

Data security and privacy concerns

Data is both a valuable asset and a potential liability in the digital age. For BaaS platforms, safeguarding customer data against breaches is paramount, given the sensitive nature of financial information. The Indian IT Act and the proposed Personal Data Protection Bill highlight the importance of data security and privacy. BaaS providers must ensure robust encryption, secure data storage, and privacy-compliant operations to build user trust and comply with regulations. The challenge lies in implementing these measures without compromising user experience or operational efficiency.

Standardization and interoperability challenges

The effectiveness of BaaS hinges on the seamless interaction between different financial services and platforms. However, the lack of standardization in APIs and the varying degrees of digital readiness across banks and fintech companies can hinder interoperability. Establishing common standards and protocols is crucial for enabling smooth integrations, facilitating innovation, and ensuring a consistent user experience across services. The challenge is to bring diverse stakeholders together to agree on and adopt these standards.

Legacy systems and integration complexities

Many traditional banks in India operate on legacy systems not designed for the digital era. Integrating these systems with modern BaaS platforms involves significant technical and operational challenges. Legacy systems often come with limitations in scalability, flexibility, and security, making seamless integration a complex task that requires substantial investment in time and resources. The challenge for banks and BaaS providers is to manage this integration in a way that minimizes disruption to existing services while paving the way for future innovations.

Financial infrastructure and scalability considerations

As BaaS aims to democratize access to financial services across India’s vast and diverse market, the underlying financial infrastructure must be capable of supporting this ambition. This includes the digital platforms and the physical infrastructure like internet connectivity and mobile network coverage, especially in rural and semi-urban areas. Scalability is a critical consideration, as BaaS platforms must be designed to handle variations in demand, accommodate a growing number of users, and support the launch of new services without degradation in performance.

Talent and skill gap

The development, management, and scaling of BaaS solutions require a workforce with specialized skills in fintech, cyber security, regulatory compliance, and digital innovation. However, a notable gap exists in the availability of such skilled professionals in India. Bridging this talent gap involves attracting talent from other sectors and geographies and investing in education and training programs.

Emerging technologies to overcome BaaS challenges

Emerging technologies are pivotal in addressing the current obstacles within the BaaS landscape.

- Blockchain technology, for instance, is crucial in enhancing security and transparency through its immutable transaction ledger, fostering trust and minimizing fraud.

- AI and ML are instrumental in simplifying the integration with legacy systems, utilizing predictive analytics and intelligent automation to refine operations and craft personalized customer journeys.

- Cloud computing offers a resilient and scalable solution capable of meeting the escalating demands of BaaS platforms, thus ensuring efficient management of India's diverse market needs.

- The evolution of API management tools promotes improved standardization and interoperability across financial services, facilitating smoother collaboration and innovation.

- Automation platforms emerge as a significant force, optimizing routine processes and reducing manual errors, elevating operational efficiency.

Collectively, these technological advancements not only aim to resolve existing BaaS challenges but also lay the groundwork for a financial ecosystem that is more inclusive, secure, and focused on the customer.

Conclusion

The journey of BaaS in India has been phenomenal until now. By leveraging the power of APIs and emerging technologies like cloud computing, blockchain, and artificial intelligence, BaaS is breaking down traditional banking barriers, making financial services accessible to every corner of India. This transformative model has the potential to reshape the Indian financial landscape, offering a future where financial empowerment and innovation go hand in hand.

As we stand on the brink of this digital revolution, the promise of BaaS extends beyond mere convenience, heralding a new era of economic growth, inclusivity, and interconnectedness. The road ahead for BaaS in India is bright, filled with opportunities to redefine banking for millions, making it more personal, secure, and seamlessly integrated into our daily lives.