Since the early 2000s, India's financial sector has embarked on a digital transformation journey marked by the advent of online banking and ATM services. This transformation has gained remarkable momentum in recent years, fueled by enhanced digital infrastructure, a surge in demand for digital financial services, a booming fintech ecosystem, and supportive government initiatives.

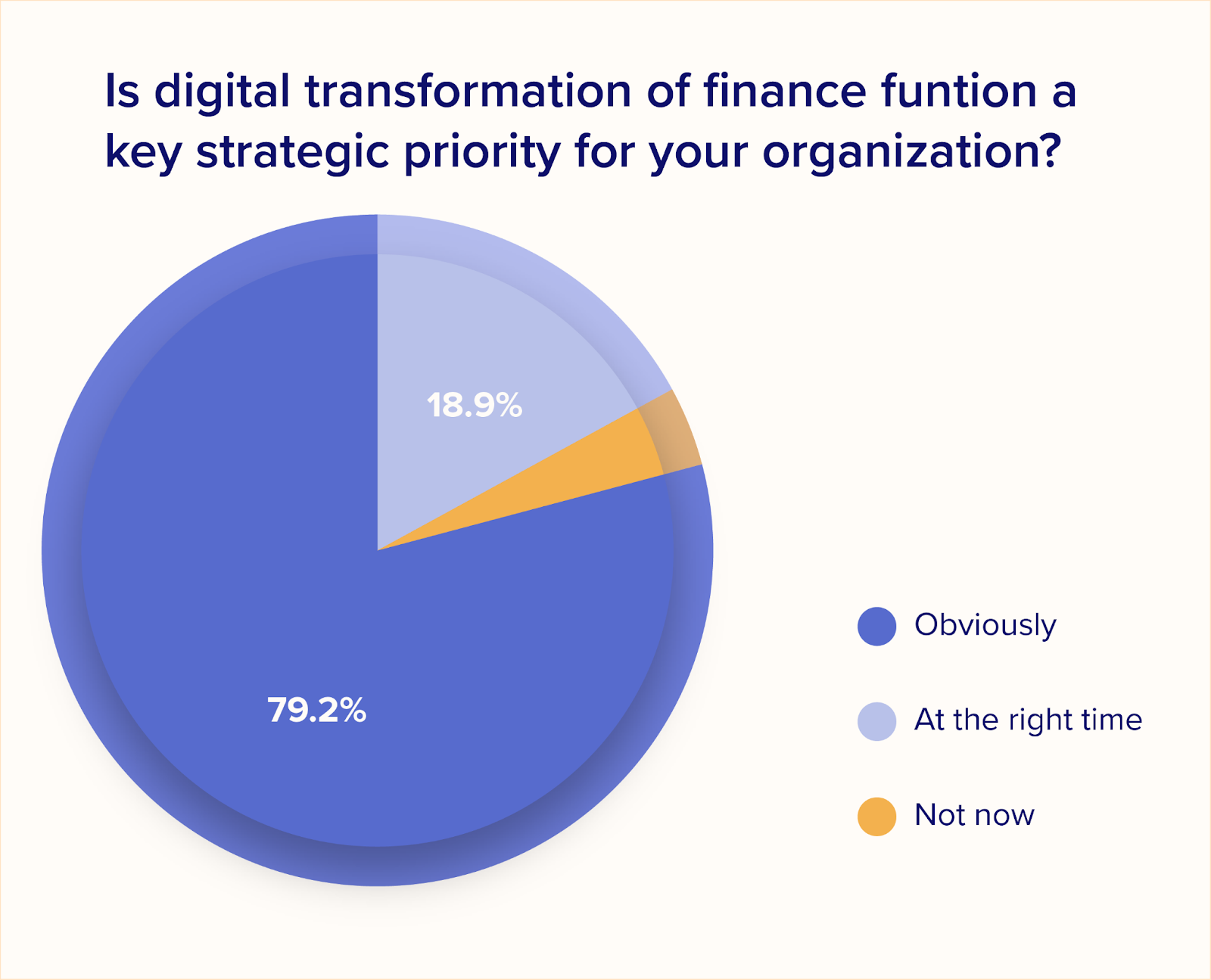

Today, digital transformation is more than a buzzword. As per a survey conducted amongst over a thousand finance leaders from across India, almost 80% agreed that the next phase of digital transformation is their strategic priority.

Defining digital transformation in finance - Beyond mere technology adoption

Digital transformation in finance goes far beyond simply implementing new technology. It is a shift in how financial institutions operate and interact with customers. This encompasses several key pillars:

Reimagining processes

Successful digital transformation demands not just replacing paper trails with automated processes but also leveraging data analytics to optimize decision-making and building modular systems that can easily adapt to evolving market conditions. Imagine seamlessly opening an account online, instantly resolving disputes through AI-powered chatbots, or receiving personalized financial advice based on real-time data analysis – these are all outcomes of a process-driven transformation.

Keeping a customer-centric approach at the core

A truly digitally-advanced financial service provider can actively listen to their customers' needs, understand their pain points, and tailor products and services to their preferences. Whether it's developing intuitive mobile apps, offering personalized financial insights, or providing 24/7 omnichannel support, every digital initiative should focus on enhancing the customer experience and building deeper relationships.

Embracing digital-first strategies

The brick-and-mortar model, while still relevant, can no longer be the sole focus. Digital transformation necessitates a shift towards digital-first thinking. This means investing in robust, secure online platforms, prioritizing mobile accessibility, and exploring innovative solutions like biometric authentication. It's about recognizing that customers expect convenience, speed, and personalized experiences and delivering them where they demand them most – in the digital realm.

In this whole technological shift, the role of integrations is pivotal. In this blog, we delve into how integrations unlock new possibilities for financial institutions in India.

Challenges in the digital transformation of financial institutions in India

On their way to digital advancement, financial institutions in India are fraught with many challenges, ranging from infrastructural hurdles to regulatory and cultural obstacles. Here are the key challenges:

- Legacy systems and infrastructure: Many financial institutions in India operate on outdated legacy systems that are incompatible with new technologies. Upgrading these systems is costly and complex, requiring significant time and resources.

- Regulatory compliance and security concerns: The financial sector in India is highly regulated. Ensuring compliance with the evolving regulatory framework while adopting new technologies can be challenging. Additionally, with the increase in cyber threats, maintaining high levels of security during the digital transformation process is paramount.

- Data privacy and protection: With the General Data Protection Regulation (GDPR) in Europe setting a precedent, India’s own data protection laws are becoming stricter. Financial institutions must navigate these regulations carefully, ensuring customer data privacy and security without hindering digital transformation.

- Digital literacy and customer trust: While there is a growing trend of digital adoption among consumers, a big portion of the population with limited digital literacy still exists. Building trust in digital services among these customers, especially in rural and semi-urban areas, is challenging.

- Workforce reskilling and cost: Reskilling the existing workforce to adapt to new digital technologies requires significant investment in training and development programs. Moreover, the associated costs of such reskilling efforts and the investment in new technology infrastructures are a deterrent.

- Change management within organizations: Transforming the organizational culture to embrace digital change, breaking down silos within the institution, and promoting agility and innovation can be challenging. Employees at all levels must adapt to new working methods, which requires comprehensive training and change management efforts.

Integrations - The key to digital transformation

Integrations facilitate a streamlined and efficient information ecosystem by breaking down data silos and enabling seamless information flow. Financial institutions can strategically leverage integration technologies to overcome the existing barriers to digital progress. Here’s how:

Modernizing legacy systems through integration with APIs

API integration serves as a bridge allowing legacy systems to seamlessly connect with modern technologies, facilitating cost-effective and less complex upgrades. This approach also helps them to future-proof their technology infrastructure and allows them to retain the robustness of their existing systems while gaining the flexibility and scalability offered by modern technologies.

Related read: Open banking APIs: Enabling fintech collaboration in India

Integrating core banking systems with third-party applications

Integrating core banking systems with third-party applications, such as payment gateways and wealth management platforms, extends the services offered to customers. This enhances the customer experience by providing a one-stop solution for various financial needs and positions the institution as a competitive player in the market.

Linking internal systems with external data sources

Integrating internal systems with external data sources, including credit bureaus and social media platforms, enriches customer profiles with a wealth of external data. This comprehensive view enables more informed risk assessment, personalized marketing, and tailored product offerings, elevating the customer experience and improving risk management.

Automating compliance and enhancing security

Integration platforms enhance security and streamline compliance by embedding checks and protocols into data exchanges, ensuring adherence to regulatory standards. They automate compliance processes, simplifying adaptation to new regulations while maintaining robust security. Furthermore, these platforms enforce strict data privacy controls and encryption, protecting customer data according to the latest standards, such as GDPR. This approach efficiently manages consent and data access, providing financial institutions with a secure and compliant data environment.

Benefits of integrations in the financial sector

By enabling different systems and technologies to work together seamlessly, financial institutions can unlock a host of benefits that propel them towards achieving their strategic goals.

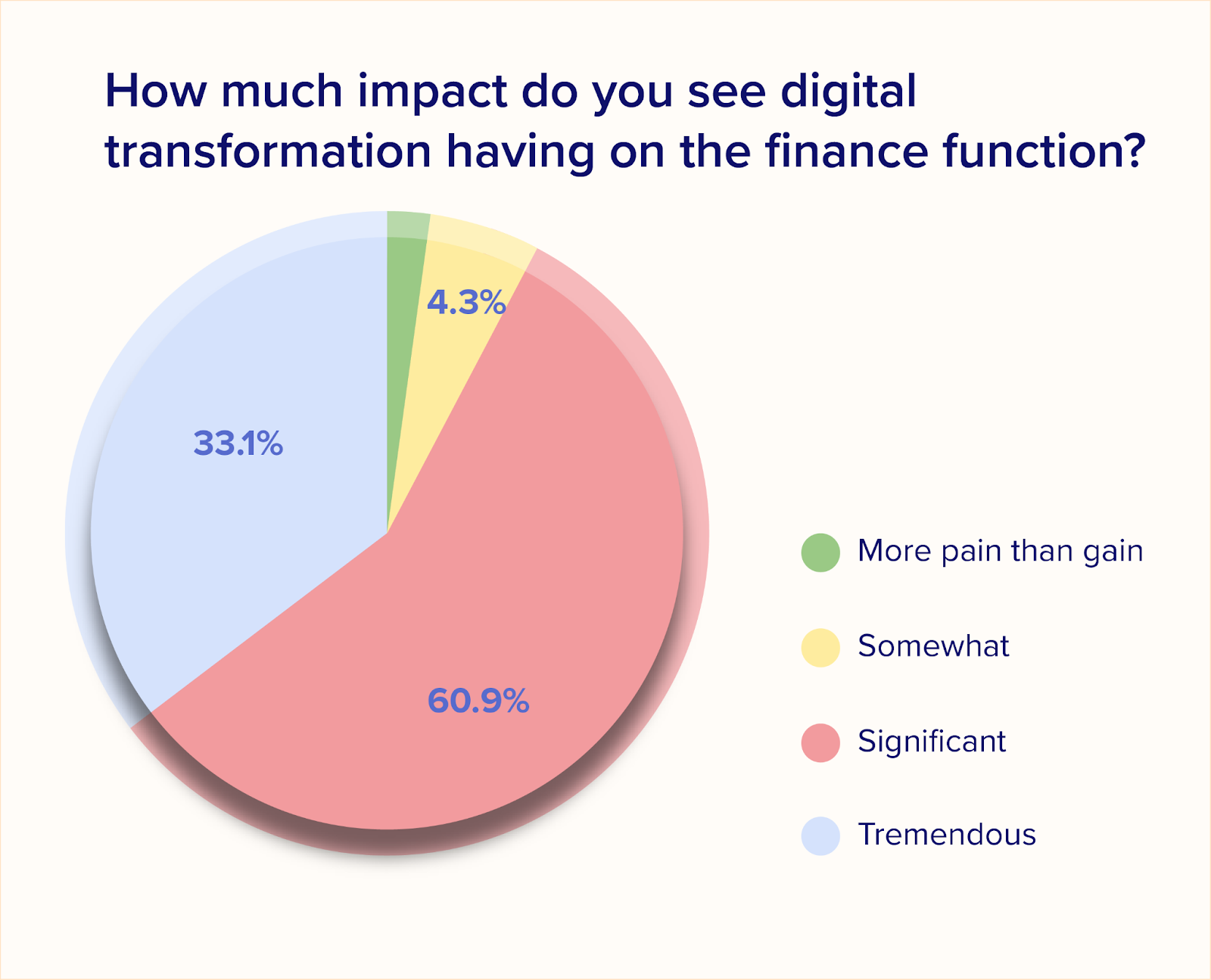

In the same survey quoted earlier in the blog, more than 90% of the leaders agreed that digital transformation significantly impacts the finance function. And integrations enable this transformation.

Here are the key advantages of embracing integrations:

Improved customer experience

- Personalized offerings: Integrations allow financial institutions to aggregate data from various sources, enabling a deep understanding of customer preferences and behaviors. This data-driven insight facilitates the creation of personalized financial products and services, tailored to meet the unique needs of each customer.

- Faster transactions: By integrating payment systems with banking applications, transactions can be processed more quickly and efficiently, reducing wait times for customers. This speed and convenience enhance customer experience, fostering loyalty and satisfaction.

Enhanced operational efficiency

- Automated Processes: Integrations streamline operations by automating routine tasks, from customer onboarding to transaction processing. This automation reduces manual intervention, increasing efficiency and allowing staff to focus on more strategic activities.

- Reduced Errors: With automated processes comes a significant reduction in human error. Integrations ensure that data is accurately transferred across systems, minimizing the risk of mistakes that can lead to customer dissatisfaction and operational losses.

Strengthened risk management

- Real-time data insights: Integrations facilitate the real-time analysis of transaction data and customer activity, enabling financial institutions to identify and respond to potential risks promptly. This capability is crucial for detecting unusual patterns that may indicate fraud or financial crime.

- Fraud detection: Advanced integration of AI and machine learning models with financial transaction systems can significantly enhance fraud detection capabilities. By continuously learning from transaction data, these systems can detect anomalies and potential fraud with greater accuracy, protecting both the institution and its customers.

Innovation opportunities

- Data-driven product development: Integrations provide access to a wealth of data that can inform the development of new financial products and services. This data-driven approach ensures that institutions can innovate in ways that meet the evolving needs of their customers.

- Collaboration with fintech: Integrations enable traditional financial institutions to easily partner with fintech companies, leveraging their technologies and innovations to enhance their offerings. Such collaborations can lead to the development of groundbreaking financial solutions that combine the strengths of both partners.

Conclusion

For financial institutions in India, embracing integrations is not merely a step towards modernizing operations but a strategic move to secure a competitive edge in a rapidly evolving digital world. The seamless integration of systems and technologies facilitates a myriad of benefits, from enhancing customer experiences with personalized and faster services to improving operational efficiency through automation and reduced errors.

The ability to adapt and innovate, powered by effective integrations, is what will differentiate leaders in the financial sector. As customers continue to demand more personalized, efficient, and secure services, institutions that leverage integrations to meet these expectations will not only thrive but also lead the way in digital transformation.