In recent years, the increased movement of goods, services, capital, and people across international borders has significantly boosted the economic relevance of cross-border payments. This surge is closely tied to the globalization of economies and the digital revolution, which have made international transactions more frequent and essential than ever. As businesses and individuals increasingly operate on a global scale, the demand for efficient, secure, and fast payment methods has risen sharply.

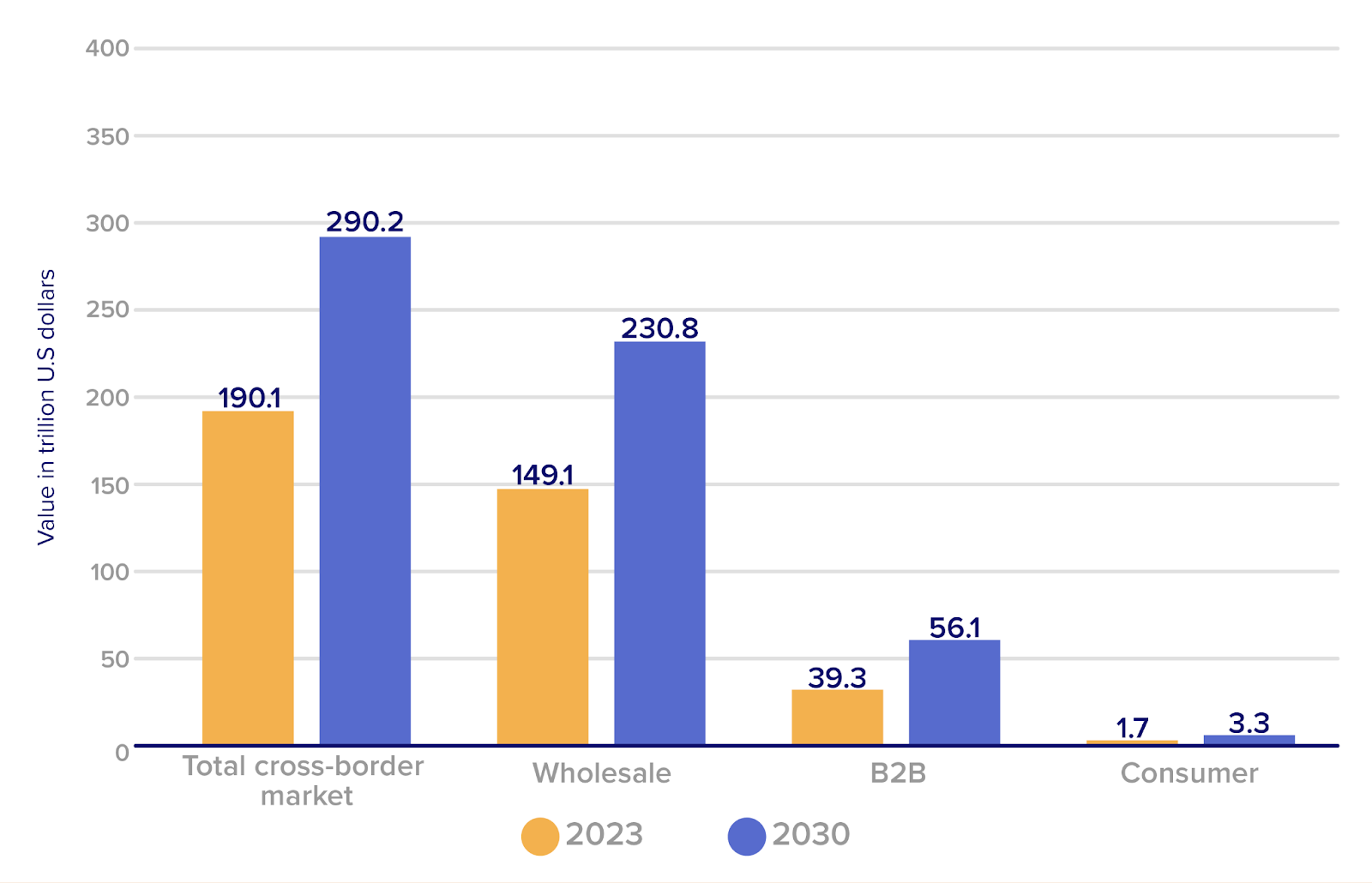

The total value of global cross-border payments is predicted to increase by over 65% by 2030 to $290.2 trillion. The chart below shows the global wholesale, B2B, and B2C market values, and their projected values over the next 7 years.

This growth is largely fueled by advancements in technology, with APIs at the core, which are set to revolutionize how payments are processed internationally. APIs facilitate seamless and instantaneous transactions, making cross-border payments more accessible and less cumbersome. In this blog, we will delve into the pivotal role of APIs in enhancing and facilitating cross-border payments, underscoring their growing importance in the global financial landscape.

Understanding cross-border payments

Cross-border transactions are financial exchanges across national boundaries involving parties from different countries. These transactions form the backbone of the global economy by supporting international trade, investments, and remittances, ranging from multinational corporations making billion-dollar deals to individuals remitting money to their families. Cross-border payments can be broadly categorized into two types:

- Wholesale cross-border payments: They are large-value transactions between banks or financial institutions, often for corporate clients or financial trading, characterized by their high value and low volume.

- Retail cross-border payments: They involve lower-value transactions between individuals or businesses across countries, such as remittances, online purchases, and tuition fees, noted for their high volume but lower value.

Complexities in cross-border transactions

Cross-border transactions are much more complicated than domestic ones, tangled in the rules, economic factors, and technology that control international finance.

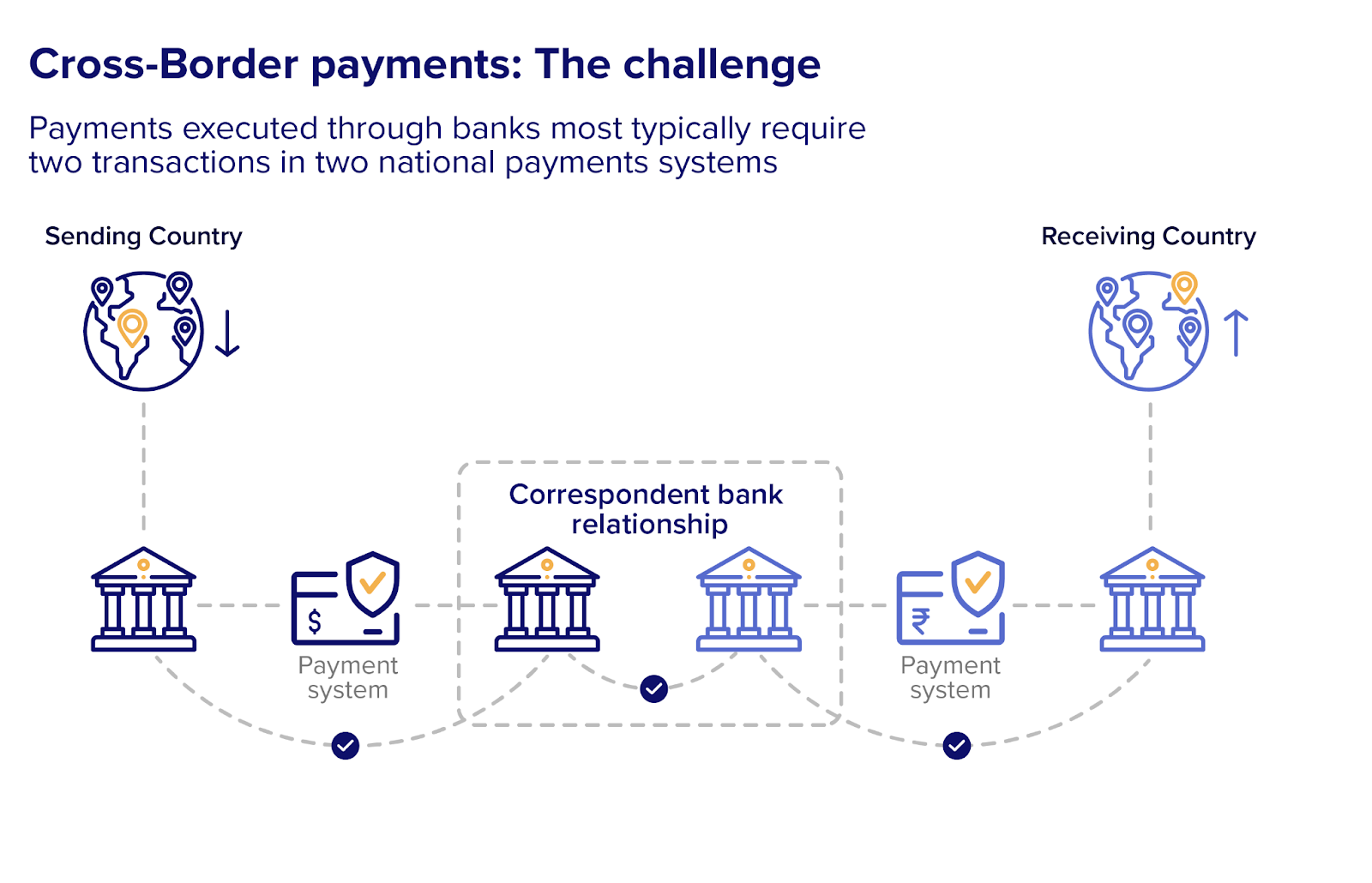

- Complex transaction chains: The traditional cross-border payment pathway involves several intermediaries, including the originating bank, correspondent banks, and the beneficiary bank. Each link in the chain adds the potential for delays, errors, and additional fees.

- Diverse legal frameworks and compliance: Each country has unique laws and regulations for international financial transactions. Navigating this maze of anti-money laundering (AML), counter-terrorism financing (CTF) laws, and cross-border trade regulations requires extensive knowledge and resources, making compliance a significant challenge. Ensuring compliance with these regulations demands rigorous due diligence processes, reporting, and record-keeping, which can be resource-intensive and time-consuming. Non-compliance risks hefty fines and legal repercussions, adding a layer of risk to cross-border transactions.

- Exchange rate volatility: Fluctuating exchange rates can significantly affect the final amount received by the beneficiary, introducing financial risk into transactions. Dealing with these uncertainties requires sophisticated financial instruments to hedge against potential losses.

- Conversion costs: Each currency conversion incurs costs, including transaction fees and less-than-optimal exchange rates offered by intermediaries. These costs can erode profit margins, particularly affecting small and medium-sized enterprises (SMEs) and individuals who lack the bargaining power to secure better rates.

Challenges in cross-border transactions

Navigating the complexities of cross-border payments presents challenges, highlighting the need for more streamlined, secure, and inclusive financial transactions on a global scale.

- Transparency, control, and reconciliation challenges: The involvement of multiple intermediaries in cross-border payments makes it difficult to track transactions and resolve disputes efficiently. This lack of transparency complicates the reconciliation of payments with their corresponding invoices, especially when faced with information mismatches or delays.

- Security risks and compliance requirements: The intricate network of parties and systems increases the exposure to fraud and security breaches, necessitating sophisticated security measures. Additionally, ensuring compliance with international data protection regulations, such as GDPR, introduces further complexity into the transaction process, requiring stringent data handling and protection protocols.

- Technological and infrastructure disparities: Differences in technology and payment infrastructures across countries lead to inefficiencies, incompatibility, delays, and errors, in the payment processes.

- Access, inclusion, and payment limitations: Ensuring that smaller businesses and individuals have access to cross-border payment systems is essential, yet many face barriers due to limited resources or infrastructure. Moreover, navigating restrictions on payment amounts, transaction types, or permissible countries—imposed by regulatory bodies or financial institutions—further complicate seamless cross-border transactions.

The role of APIs in cross-border payments

APIs have become a cornerstone of innovation in the financial sector, including facilitating cross-border payments. They enable seamless integration, real-time operations, and compliance adherence. By leveraging APIs, financial services can bypass traditional, cumbersome processes, making international transactions faster, cheaper, and more transparent.

Incorporating APIs into the infrastructure of cross-border payments directly addresses most challenges and complexities that have traditionally plagued international transactions.

Direct connection and automation for payment networks

APIs create direct connections between payment networks, financial institutions, and businesses, enhancing payment initiation precision. By using real-time data for currency conversion and ensuring compliance, APIs make international transactions faster and more cost-efficient, fueling global e-commerce growth.

Real-time financial management enhancement

International money transfer APIs grant corporate treasurers and finance departments real-time access to foreign exchange rates. This immediate insight aids in managing currency risks and making informed decisions, optimizing currency pricing, and cutting transaction costs.

Efficient payment routing

APIs analyze multiple payment routes in real-time, and ensure that payments are processed through the path that offers the best combination of speed, cost, and reliability. This capability not only enhances the efficiency of transactions but also reduces potential delays and costs associated with traditional routing methods.

Transaction tracking and analytics in real-time

Using APIs, businesses and individuals receive instant updates on transaction statuses, promoting transparency. This real-time tracking and analysis are vital for refining payment strategies and boosting customer satisfaction.

Seamless payment functionality integration for businesses

APIs enable businesses of all sizes to integrate diverse payment options into their systems, from digital currencies to recurring payments. This adaptability encourages innovation and gives businesses a competitive edge by allowing custom payment solutions.

Data security and compliance

APIs prioritize security and compliance in cross-border payments by securing data transfers and enforcing strict authentication. They also automate compliance tasks like identity verification and anti-money laundering checks, enhancing transaction security. They provide insights into customer behavior, supporting compliance with international standards and broadening customer outreach.

Global commerce enhancement through marketplace integration

APIs simplify customer verification and currency conversion by integrating with KYC and FX service providers. This enhances the marketplace experience with faster fund disbursement and transparent, multi-currency transactions, facilitating global trade.

Conclusion: Navigating the future of cross-border payments

The battleground of cross-border payments has seen fintech firms making significant strides against traditional banks. As fintechs continue to disrupt the market with their digital-first solutions, banks are increasingly recognizing the need to embrace new technologies and reimagine their business models. The strategic emphasis is shifting towards creating digital propositions that can compete on speed, cost, and user experience.

The growth of APIs and the adoption of new technologies like blockchain and DLT underscore a broader industry movement towards more efficient, secure, and customer-centric payment solutions.

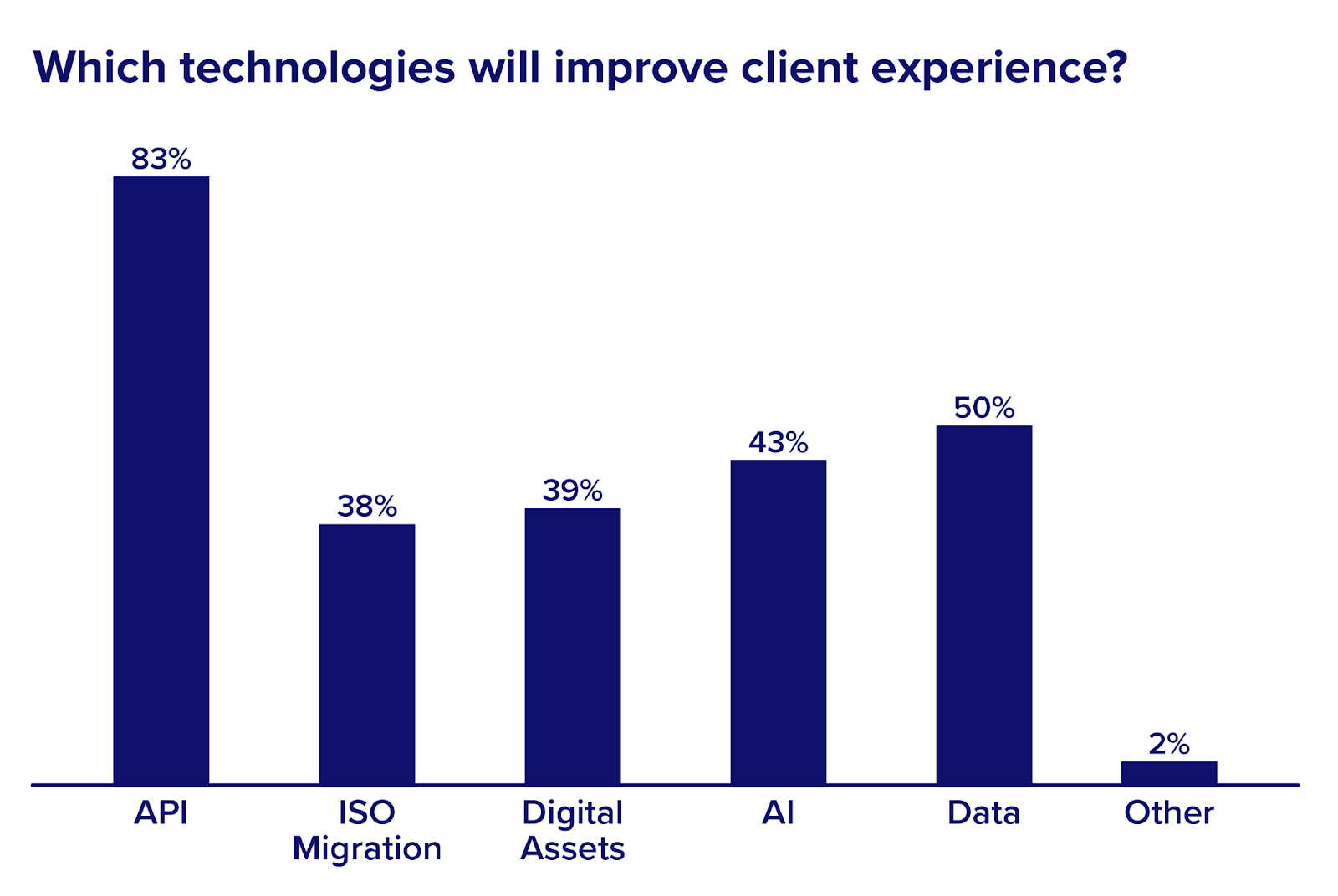

As per this report by Citi on the future of cross-border payments, 83% of banks consider APIs as the key technology enabler in cross-border payments, allowing them to expand their network through partnerships with connectivity providers, elevate their capabilities, and deliver true digital client experience.

As we look towards 2030, the landscape of cross-border payments is set to be characterized by a blend of competition and cooperation, driving the industry towards a more interconnected and inclusive global financial ecosystem.